Last week the Spanish energy giant Repsol announced its new strategic plan which involves selling off assets and sharply reducing capital spending. In announcing its new plan Repsol follows its larger rivals Exxon-Mobil, Shell and BP that have announced reductions in capital spending and/or headcount in the last few months as a result of the very real possibility that oil proices will continue to be low for some time to come.

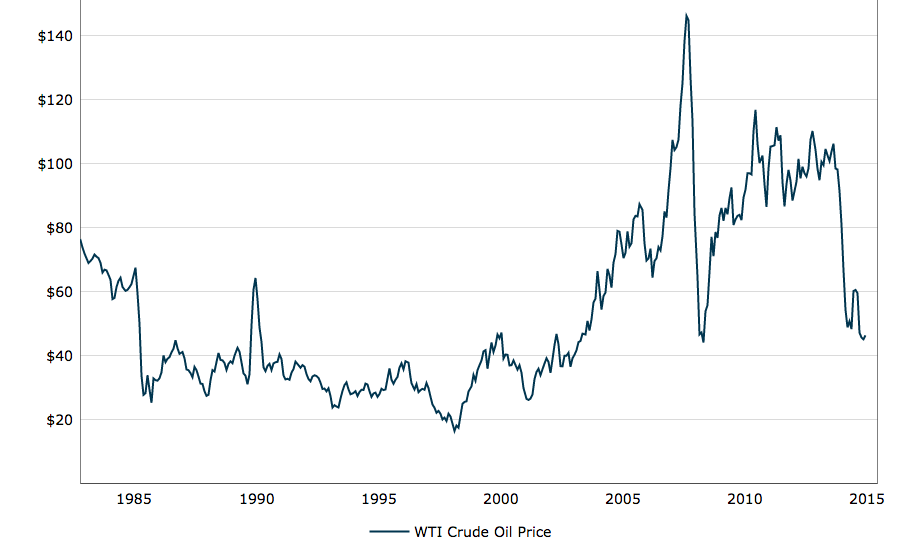

The issue is that from June, 2014 to December, the benchmark oil price dropped from approximately $ 120 per Barrel to just over $50. West Texas Intermediate was trading today at $ 47 and Brent just over $48. As a result of the drop in price, a number of large energy companies saw their valuations drop which allowed Shell, for example to buy BG Group and Repsol to acquire Talisman, a Canadian company which was struggling to pay its debts at the lower price.

The problem is that almost a year later we are looking at a potentially long lasting restructuring of the global energy sector which is struggling to maintain profitability at the current low price of oil.

How Low Can It Go?

In their latest report on this issue, Goldman Sachs is actually managing a scenario where oil could drop to as low as $20 per barrel and the report hit headlines around the world when it came out. I recommend the 3 minutes summary of the report that you can see below.

In my view, the initial drop in price was deliberately caused by Saudi Arabia which used its excess capacity to depress prices below the level at which shale gas and so called marginal oil wells were profitable. Such projects are thought to break even at or around $60-70 per barrel and the idea I believe was to drop the price below that level in order to curb the enormous boom in energy production in the United States.

The U.S. has been for many years the world’s largest net importer of oil but its imported volume has dropped form a high of 12 million barrels per day in 2007 to just over 5 million in 2014. If the trend were to have continued then the U.S. would have become a net exporter of energy in the next few years.

What the Goldman Sachs report highlights is that many of the investments in the U.S. have already been made and thus the production will most likely stay on line for the foreseeable future. This capacity as well as the need for non opec members such as Russia and Venezuela to keep selling oil at whatever price they can has led to a drastically different situation which has no clear end in sight.

A Good Thing?

While for consumers and many industries, low energy prices are clearly a good thing there are serious ecological and geo-political issues which are worth thinking about. In the first place low prices for oil and gas will make it harder for wind and solar energy to compete despite the incredible cost reductions these technologies are experiencing as the they begin to reach scale. Secondly, low energy prices might make it more difficult for the world to agree on ambitious targets to reduce CO2 emissions in the Paris climate talks in a few weeks.

In geo-political terms, many of the countries in the Persian gulf rely on oil sales to subsidize their economies and bring some semblance of prosperity to their citizens. Without sufficient income, they may be forced to cut social services and thus provide arguments for the radicals on both sides of the Shia, Sunni divide who seek a redistribution of wealth and political power.

How Long?

I actually was working as an engineer in Houston’s oil sector in 1984 and I remember when the price of oil dropped by 60% causing many of us to lose our jobs. For me things worked out well because the crash gave me the push I needed to come and do my MBA at IESE. The thing is that despite a spike in the Fall of 1990, oil prices did not recover for 20 years when adjusted for inflation and perhaps history will repeat itself.