IESE Library

Library Survey 2024Students

Global Risks

Newsletter Nº. 103

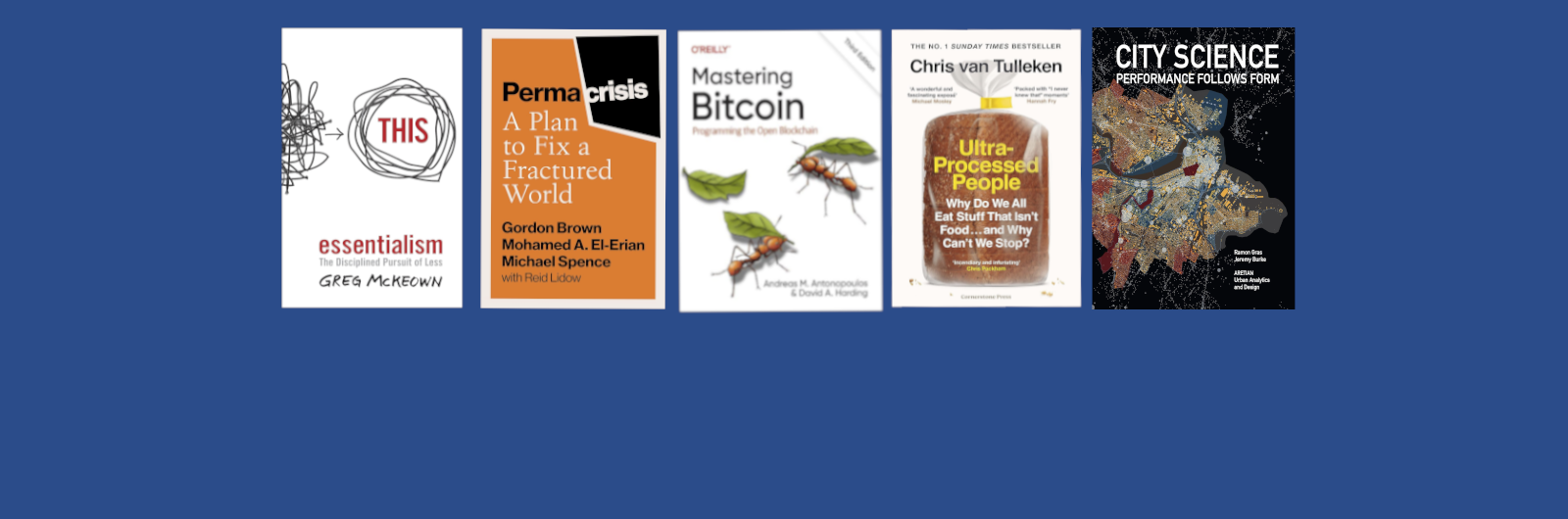

New Books

Top Databases

Contact info

Barcelona

-

IESE Library (G-100)

Avenida Pearson, 21

08034 Barcelona. España -

+34 93 253 42 00 (ext. 504423)

library@iese.edu

Madrid

-

IESE Library

Camino Cerro del Águila, 3

28023 Madrid. España -

+34 91 211 30 00 (ext. 513215)

library@iese.edu

Join us