In this, the second of three posts on shale gas, I want to focus on the impact that fracking technology and shale gas is having on the international energy business. There will, in fact, be a panel on the topic at the upcoming Good Doing Well Conference at IESE on February 21st and 22nd.

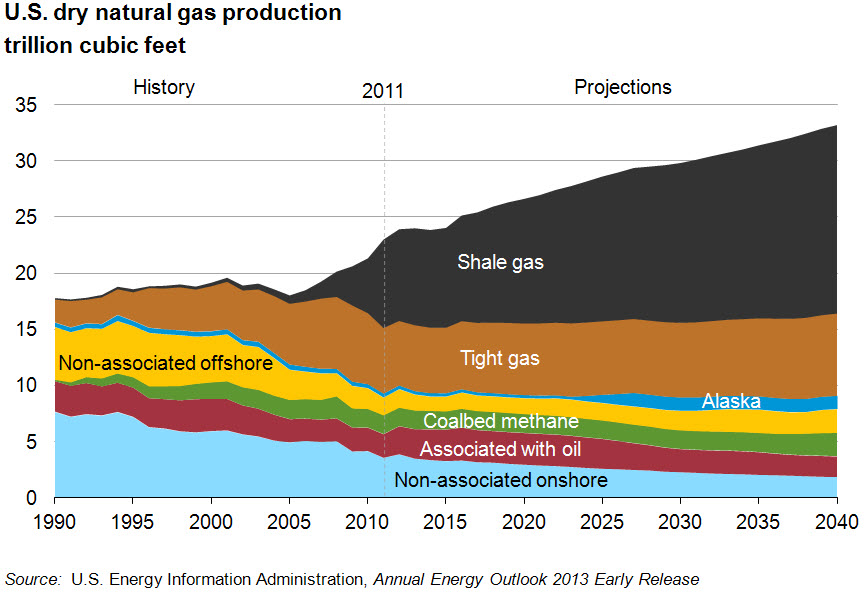

Over the last three years, the Unites States has continued to produce and market over 20 trillion cubic feet of natural gas surpassing record production set in 1973. As shown in the chart above which is provided by the U.S. Energy Information Administration (EIA), shale gas represent only a part of that production but is the part that is setting the records and changing the game.

In my view the key impact of shale gas on the global energy business is its impact on wind and solar energy and its impact on the worldwide price of gas.

Headwinds for wind

The low gas price has sharply reduced the prospects for wind Energy in the U.S. As mentioned last week, spot prices for gas at Henry Hub are just over $4 per million BTUs, and conventional wisdom puts grid parity for wind at somewhere around $5 when compared head to head with natural gas. Bloomberg reported back in October that 2013 would be a terrible year for the industry and reach levels significantly below the 13 Gigawats installed in 2012 due to expiring federal tax incentives. The larger issue is that the industry has also had trouble in Europe and while many people including myself believe in the long term prospects for wind, the share prices of both Vestas and Gamesa which have been recovering lately, are still well below their pre-crisis highs.

The low gas price has sharply reduced the prospects for wind Energy in the U.S. As mentioned last week, spot prices for gas at Henry Hub are just over $4 per million BTUs, and conventional wisdom puts grid parity for wind at somewhere around $5 when compared head to head with natural gas. Bloomberg reported back in October that 2013 would be a terrible year for the industry and reach levels significantly below the 13 Gigawats installed in 2012 due to expiring federal tax incentives. The larger issue is that the industry has also had trouble in Europe and while many people including myself believe in the long term prospects for wind, the share prices of both Vestas and Gamesa which have been recovering lately, are still well below their pre-crisis highs.

High Priced Miscalculations

In 2007, Nigeria LNG put its sixth LNG compression train in operation at a reported cost of $ 1.7 Billion and even larger investments were made in Qatar and Australia in recent years due to a perceived increase in demand for gas in Europe, China, and the United States.

What seems to be driving much of the demand is the expectation that gas prices will be lower and perhaps less volatile than oil due to larger reserves and the added benefit of producing about a third less greenhouse gases than oil and just over half as much as coal.

The problem, is that with the U.S. rapidly approaching independence the balance of trade in LNG might shift and in Quintana Texas a company is making a $ 13 billion investment to create an LNG liquefaction plant. There is some debate on the issue and an industry lobby called America’s Energy Advantage is actively trying to get the Department of Energy to not allow gas exports.

Global Impact

Regardless of how much shale gas is exported from the U.S. and the impact that cheaper gas has there, the other factor has been to put some limits in gas prices around the world as producers have had to find outlets for their gas and have largely been flat according to the International Gas Union in its 2013 report.